Jai Corp Ltd. - ???

There are two striking things about Jai Corp Ltd.'s balance sheet -

a) It has a net current asset of 140.56 crs (i.e. 162.9 rupees per share)

b) It has investments of 57.87 crs (i.e. 67.1 rupees per share)

Add a) and b), you find a Grahamian NCAV at 230.0 rupees per share. The stock is available today (Feb-26) at 109.90 on the NSE - a discount of 52.21% on the NCAV !!!

On further examination of the investments, the company has been a rather decent participant at the stock markets. As of 31-Mar-2005, it held the following shares :

1. Bharati Shipyard - 10728 shares - Today: 383 rupees = 0.41 crs

2. Jet Airways - 8592 shares - Today: 964 rupees = 0.82 crs

3. ONGC - 159975 shares - Today: 1175 rupees = 18.79 crs

4. PNB - 11199 shares - Today: 452 rupees = 0.51 crs

5. Indraprastha Gas - 110000 shares - Today: 138 rupees = 1.51 crs

6. TCS - 33538 shares - Today: 1687 rupees = 5.65 crs

Thus, the total quoted investments itself comes to 27.71 crs i.e. rupees 32.1 per share

A discount of 52.51% on NCAV - seems a cropper !!!

What I dont like about the stock?

a) Reducing Q-on-Q sales and profits

b) The company has charged taxes at -1.30, -1.14 and -0.52 for the three quarters of this year

c) The company is striving to get it's cash liquidity in place

See Chart (you'll be surprised that the stock has not gained much over the last 1.5 years, while the market has gone crazy .. including peers of Jai Corp Ltd.

Im confused on this one !!!

a) It has a net current asset of 140.56 crs (i.e. 162.9 rupees per share)

b) It has investments of 57.87 crs (i.e. 67.1 rupees per share)

Add a) and b), you find a Grahamian NCAV at 230.0 rupees per share. The stock is available today (Feb-26) at 109.90 on the NSE - a discount of 52.21% on the NCAV !!!

On further examination of the investments, the company has been a rather decent participant at the stock markets. As of 31-Mar-2005, it held the following shares :

1. Bharati Shipyard - 10728 shares - Today: 383 rupees = 0.41 crs

2. Jet Airways - 8592 shares - Today: 964 rupees = 0.82 crs

3. ONGC - 159975 shares - Today: 1175 rupees = 18.79 crs

4. PNB - 11199 shares - Today: 452 rupees = 0.51 crs

5. Indraprastha Gas - 110000 shares - Today: 138 rupees = 1.51 crs

6. TCS - 33538 shares - Today: 1687 rupees = 5.65 crs

Thus, the total quoted investments itself comes to 27.71 crs i.e. rupees 32.1 per share

A discount of 52.51% on NCAV - seems a cropper !!!

What I dont like about the stock?

a) Reducing Q-on-Q sales and profits

b) The company has charged taxes at -1.30, -1.14 and -0.52 for the three quarters of this year

c) The company is striving to get it's cash liquidity in place

See Chart (you'll be surprised that the stock has not gained much over the last 1.5 years, while the market has gone crazy .. including peers of Jai Corp Ltd.

Im confused on this one !!!

posted by Shankar Nath at 9:17 PM

10 comments

![]()

![]()

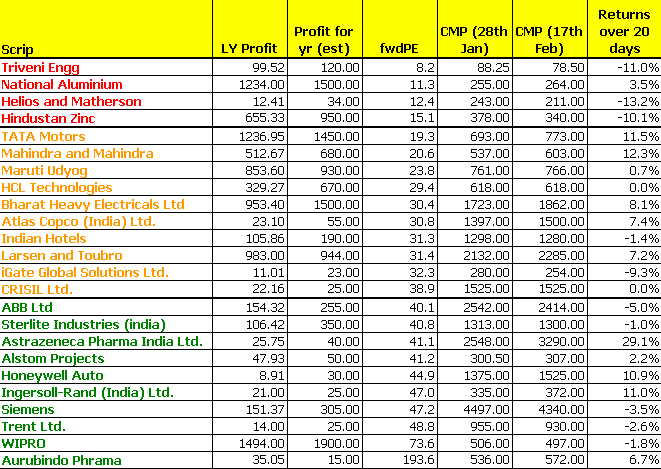

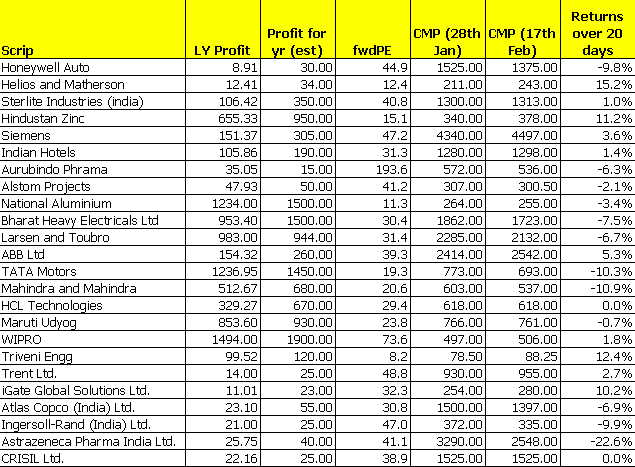

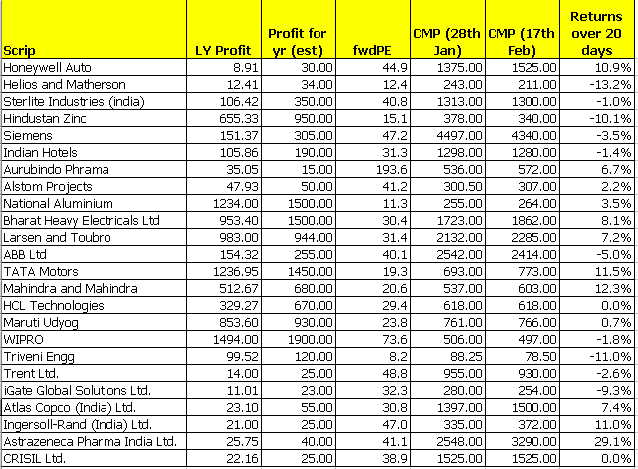

First impressions may read the following numbers -

First impressions may read the following numbers -

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}