Change is good

The recent change in conditions at HCL Infosystems is a good example of how any change in the 4Ps (price, place, product, public) can dent or raise a stock's going price.

To illustrate -

Say HCL Infosystems. Upon viewing the Q1 + Q2 data, I find that the change in agreement with Nokia, means the company has dented it's revenue numbers (ceteris paribus) by 40.12%. The new revenue number will be 3041 crores (i.e. 50% of 4074 crs from their telecom business plus 1004 crs from other businesses). The PBT would come to 115.5 crs - a dent of 32.06%. If I were to not question the fact that the HCL Infosystems stock is overly/fairly/under priced, the HCL Infosystems stock should have been at anywhere betwee 32% to 40% i.e. from a price of 259 rupees ... the fall should lie between 155 rupees and 176 rupees.

The stock had an intra-day low of 145 rupees and it closed at 180 rupees. Pricing anamoly.

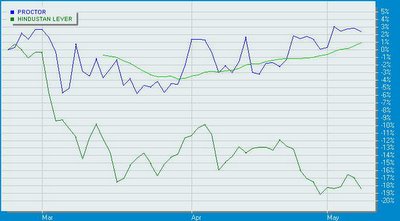

A more interesting example can be seen in the 2004 HLL-P&G price war where P&G initiated a price war by reducing the price of popular detergents by 25%. As a response, HLL followed suit with a 25% reduction in prices. The P&G scrips were at 405 on the day of the announcement and HLL stock was quoted at 174 rupees.

Surprisingly the P&G stock went upto 433 rupees by the first week of May (see charting) while the HLL stock actually reduced from it's levels by a good 18% till the first week of May (from 175 rupees to 142 rupees; HLL touched a low of 105 rupees on August 16th, 2004).

Same industry. Same reduction in price. Same effect to profitability. And yet, the 4th P (public) made a different inference.

But that's not the point .... Analyse this !!!! Detergents contributed only 24% to the total revenue of HLL. Which means the 25% reduction in price should have brought down the revenue by only (25% mult by 24%) ... 6%, but the market actually drilled down the HLL price by exactly the same amount of price cut i.e. TWENTY FIVE PERCENT.

A clear anomaly in understanding "impact on profitability".

Value investors kept on buying this stock as soon as it went below the price of 150 rupees. Easy money. Watch out for such opportunities !!!!

To illustrate -

Say HCL Infosystems. Upon viewing the Q1 + Q2 data, I find that the change in agreement with Nokia, means the company has dented it's revenue numbers (ceteris paribus) by 40.12%. The new revenue number will be 3041 crores (i.e. 50% of 4074 crs from their telecom business plus 1004 crs from other businesses). The PBT would come to 115.5 crs - a dent of 32.06%. If I were to not question the fact that the HCL Infosystems stock is overly/fairly/under priced, the HCL Infosystems stock should have been at anywhere betwee 32% to 40% i.e. from a price of 259 rupees ... the fall should lie between 155 rupees and 176 rupees.

The stock had an intra-day low of 145 rupees and it closed at 180 rupees. Pricing anamoly.

A more interesting example can be seen in the 2004 HLL-P&G price war where P&G initiated a price war by reducing the price of popular detergents by 25%. As a response, HLL followed suit with a 25% reduction in prices. The P&G scrips were at 405 on the day of the announcement and HLL stock was quoted at 174 rupees.

Surprisingly the P&G stock went upto 433 rupees by the first week of May (see charting) while the HLL stock actually reduced from it's levels by a good 18% till the first week of May (from 175 rupees to 142 rupees; HLL touched a low of 105 rupees on August 16th, 2004).

Same industry. Same reduction in price. Same effect to profitability. And yet, the 4th P (public) made a different inference.

But that's not the point .... Analyse this !!!! Detergents contributed only 24% to the total revenue of HLL. Which means the 25% reduction in price should have brought down the revenue by only (25% mult by 24%) ... 6%, but the market actually drilled down the HLL price by exactly the same amount of price cut i.e. TWENTY FIVE PERCENT.

A clear anomaly in understanding "impact on profitability".

Value investors kept on buying this stock as soon as it went below the price of 150 rupees. Easy money. Watch out for such opportunities !!!!

posted by Shankar Nath at 9:56 PM

![]()

![]()

3 Comments:

Hello dear,

I think that you are nearly correct.But you never know that when the markets will unlock the value.....anyways ur articles are really very very intresting and informative.....i think your language is beautiful..... simple and logical...

Hi ther !

What do you think about iflex scrip ? Its trading at P/e 41, Financial year closes in March. I am told that this year's revenus would be close to $380 Mn. They have a 50% /50% - product and services mix, interesting INdian company. Operating margins for their flexcube product has been historically at 48-50% and for services around 12%. THey should be growing topline at 40% as indicated earlier, from $265 Mn to around $380. What is the take on this company ? Its in a unique position in the Indian markets, no other company has such a high product revenue coming in. Especially after the Oracle acquisition of Citi's stake, strategically they are well placed to expand. Previously when they used to go to Bank of America calling themselves as Citi subsidiary they were literally thrown out. ! They are better placed now riding on the ORacle parentage and they have a good chance of riding on Larry Ellisson's sales force. I need your thoughts on this stock from its current levels and what you think could be its pricing based on current estimates. Their investor section in the website gives a fair idea. Thanks - Greyzone !

Hi Abhinav,

I guess, its difficult to say 'what happens when' most of the time. Anyways, thanks for the compliments. I just try to make things simple for people to understand. Im glad you like it.

Warm Regards, Shankar

Post a Comment

<< Home